Introduction: Service Builds Character—Credit Builds Options

Serving in the military shapes people in ways few other experiences can. Discipline, structure, responsibility, and resilience become part of daily life. Yet when it comes to personal finance—especially credit—many service members are left to figure things out on their own.

That is unfortunate, because military life actually provides a unique advantage for building strong credit.

Stable income. Predictable schedules. Federal protections. Access to specialized financial products.

When managed intentionally, these factors create one of the best environments for building credit early and building it well.

This article is written for active-duty service members, officers, enlisted personnel, and even leaders planning life after service. It approaches credit not emotionally, but strategically—the same way leaders approach missions, logistics, and long-term planning.

Because credit, like service, is not about flash.

It is about preparation, consistency, and trust.

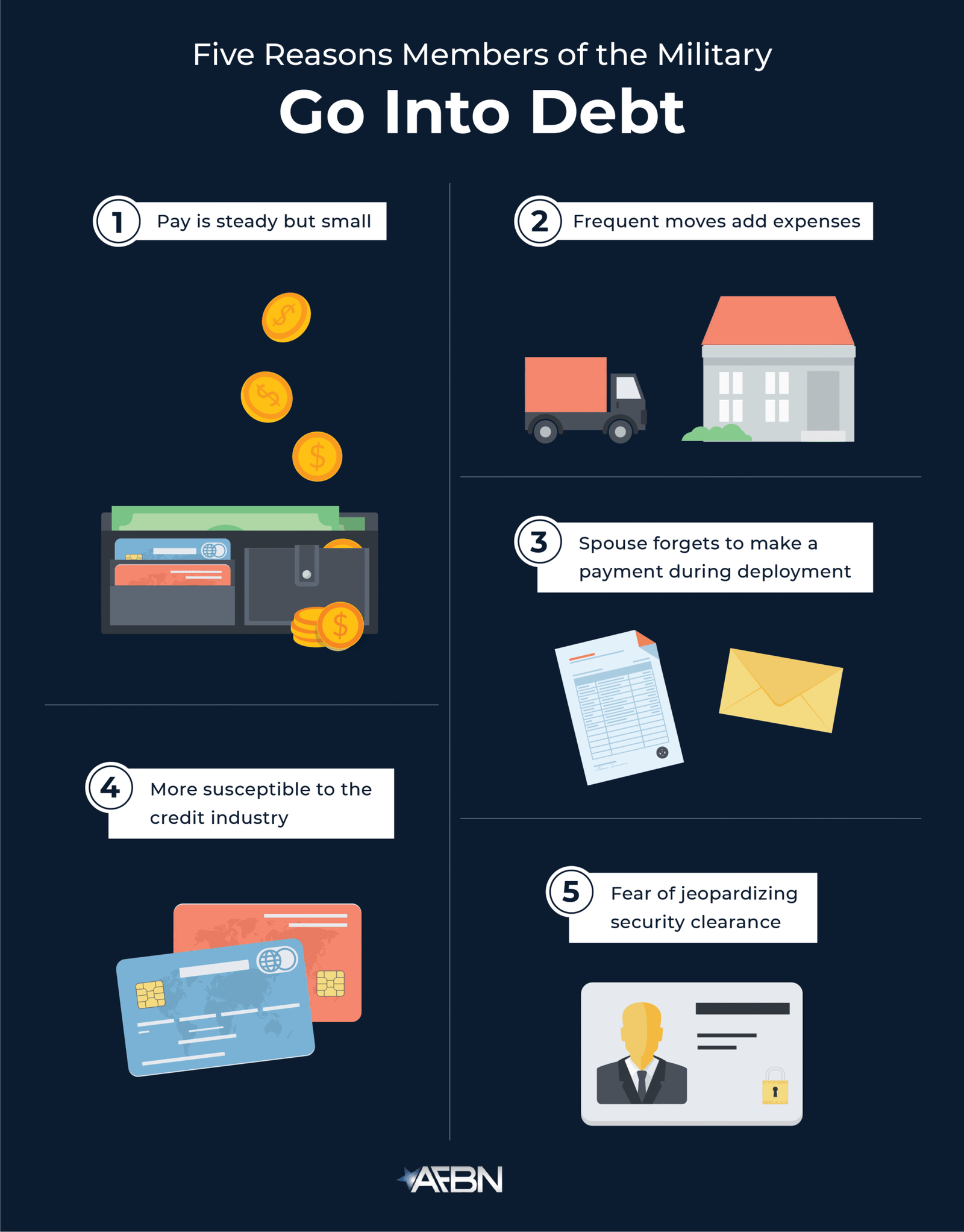

Why Credit Matters So Much for Military Members

Credit impacts nearly every major life decision a service member will face—both during and after military service.

Strong credit helps with:

- Renting or buying housing

- Purchasing vehicles

- Security clearance considerations

- Transitioning to civilian careers

- Starting a business after service

- Accessing lower-cost financing

Weak credit quietly creates friction at every step.

Military members often focus on mission readiness, but financial readiness deserves equal attention. Credit is a core component of that readiness.

Military Life and Credit: Unique Advantages Most People Miss

Military service provides structural benefits that civilians often do not have.

1. Stable, Predictable Income

Lenders value predictability more than high income. Military pay—while not always high—is reliable.

Reliability builds trust.

2. Federal Protections Under the SCRA

The Servicemembers Civil Relief Act (SCRA) provides:

- Interest rate caps

- Protection from default judgments

- Reduced financial pressure during active duty

These protections reduce downside risk when credit is used responsibly.

3. Access to Military-Friendly Financial Institutions

Banks and credit unions serving military members often offer:

- Lower fees

- Better customer service

- Products designed for service lifestyles

Used well, these institutions become long-term partners.

The Leadership Mindset: Credit Is Infrastructure, Not Lifestyle

Many young service members associate credit with consumption—cars, gadgets, or lifestyle upgrades.

That mindset limits long-term outcomes.

Strong leaders understand:

- Credit is infrastructure

- Infrastructure supports future missions

- Misused infrastructure creates bottlenecks

Building credit while in the military is not about spending more.

It is about building leverage for the future.

Step One: Establishing Credit Early and Cleanly

For many service members, military service begins around the same time as financial independence. This is the ideal moment to build credit correctly.

Open One Primary Credit Account

The goal is not variety. The goal is a clean starting point.

A single, well-managed credit card can establish:

- Payment history

- Account age

- Responsible usage

From a strategic standpoint, simplicity wins early.

Step Two: Use Credit Cards With Military Precision

Credit cards are the most effective tool for building credit during military service—when used intentionally.

Assign Credit to Predictable Expenses

Examples:

- Phone bills

- Internet

- Fuel

- Groceries

Predictable expenses reduce risk and build consistency.

Keep Utilization Low

A simple rule:

- Use less than 30% of available credit

- Pay in full every month

Low utilization signals control, not dependency.

Automate Discipline: Remove Human Error

Military operations rely on systems, not memory. Credit should be no different.

Automation ensures:

- No missed payments

- No emotional decision-making

- No unnecessary risk

Strong credit profiles are built quietly, not heroically.

Special Considerations for Deployment

Deployments introduce complexity—but also opportunity.

Prepare Before Deployment

Before deploying:

- Automate payments

- Set alerts

- Reduce balances

- Notify lenders if necessary

Preparation prevents damage during periods of limited access.

Deployment Does Not Mean Credit Pauses

Credit activity continues whether you are stateside or deployed. Discipline before deployment ensures progress continues uninterrupted.

The SCRA Advantage: Use It Wisely

The Servicemembers Civil Relief Act is a powerful safety net—but it is not a license for poor decisions.

Used wisely, it:

- Reduces interest costs

- Protects against emergencies

- Provides flexibility

Used poorly, it delays learning discipline.

Strong leaders respect safeguards without abusing them.

Avoiding the Most Common Military Credit Mistakes

Even disciplined people make predictable credit mistakes.

1. Buying Expensive Vehicles Too Early

High-interest auto loans damage credit flexibility and cash flow.

Vehicles depreciate. Credit history compounds.

2. Opening Too Many Accounts at Once

Multiple applications signal uncertainty and reduce score momentum.

3. Ignoring Credit Reports

Errors are common—and silence does not fix them.

Oversight is leadership.

Building Credit While PCS Moves Happen

Frequent moves can disrupt finances—but they do not have to disrupt credit.

Key strategies:

- Maintain the same primary bank

- Keep mailing addresses updated

- Use online banking tools

- Avoid unnecessary account changes

Consistency matters more than location.

Credit and Security Clearances: The Quiet Connection

Financial stress is a known security concern.

Strong credit does not guarantee clearance—but poor credit can raise red flags.

Rebuilding or maintaining credit demonstrates:

- Responsibility

- Stability

- Risk awareness

Credit is not just financial—it is reputational.

Preparing for Life After the Military

Whether separation is years away or approaching quickly, credit built during service compounds after service.

Strong credit enables:

- Easier housing transitions

- Lower-cost education financing

- Business startup capital

- Career flexibility

Veterans with strong credit move with confidence. Those without it face unnecessary obstacles.

Credit for Officers vs Enlisted: Same Rules, Different Contexts

Income differences matter less than behavior.

Officers often qualify for higher limits—but misuse creates bigger damage.

Enlisted members may start smaller—but consistency creates strong outcomes.

Credit systems reward discipline, not rank.

Using Credit to Build Confidence, Not Pressure

Strong credit should reduce stress, not increase it.

If credit creates anxiety:

- Simplify

- Reduce limits

- Focus on automation

Confidence comes from control, not access.

Time: The Most Underrated Military Advantage

Military service often spans years. Credit rewards time.

An account opened at 20 years old can become a powerful asset by 30—without ever carrying debt.

Time + discipline = leverage.

Monitoring Credit Like an Officer Reviews Readiness

Quarterly reviews are enough.

Check for:

- Errors

- Utilization trends

- Payment history

Do not obsess.

Do not ignore.

Leadership lives in the middle.

Credit After Mistakes: Course Correction, Not Panic

Mistakes happen—even in disciplined environments.

Late payment?

High balance?

Unexpected expense?

Correct quickly. Adjust systems. Move forward.

Credit systems forgive consistency—not excuses.

The Long View: Credit as a Veteran’s Strategic Asset

Years after service, few people remember:

- Your rank

- Your duty station

- Your unit

But credit systems remember how you handled responsibility.

Strong credit becomes:

- Quiet leverage

- Lower stress

- Greater independence

It is one of the most transferable assets military service can help build.

Final Thoughts: Serve With Discipline, Build With Intention

Military service teaches responsibility, structure, and foresight. Credit rewards the same traits.

Building credit while in the military is not about lifestyle upgrades or financial shortcuts. It is about preparing your future self—whether that future includes continued service, entrepreneurship, or civilian leadership.

Credit is not earned through words.

It is earned through behavior.

And few environments are better suited for disciplined behavior than military service.

Word Count:

514

Summary:

Most people who just join the military are in an enviable

Keywords:

navy federal credit union, nfcu

Article Body:

Most people who just join the military are in an enviable position of having very little or no established credit. While this may seem like a bad thing, it actually puts you in a great position to build good credit. It is much easier to build good credit then it is to repair it so now is the time to thoughtfully establish some and maintain it to improve your credit rating. The military offers its service people an advantage. Lenders like the fact that you will have a guaranteed paycheck for four years and are more apt to extend credit for the first time.

The first thing you should do is receive a copy of your credit report. There are three primary credit bureaus, Experian, Trans Union and Equifax that supply credit reports. It is advisable to get a credit report from all three. You will then need to analyze your report to see if it is accurate and what it says. If there are items on there that you are unaware of, now is the time to clear it up. With identity theft so prevalent today, even though you may not have credit, someone else may have gotten something in your name.

Then, you will need to open a bank account. Navy Federal Credit Union (http://www.navymoney.com), NFCU is a good place to start for United States Navy service members. It is advisable to open both a checking and savings account. This will show stability and allow you to pay bills and function much easier. Deposit your paycheck into your checking account and take a portion every pay period to put into your savings account. Do not touch the money in your savings account. Instead, let it grow and accumulate interest. Keep an eye on your checking account and do not let the balance get too low. Always balance it and make sure you do not bounce any checks.

You will want to apply for a revolving charge account. Types of credit that are good to get in the beginning are major credit cards like MasterCard, Visa or Discover. These will allow a lower interest rate and will help start you on a history of good payments. The trick is to not charge more than you can afford to pay off completely. Use the card for small purchases and pay the majority off each month. However, do not always pay it off entirely. You want to establish a good credit rating so be sure you do not pay late. Not only will it increase your interest rate and add finance charges but you will reduce your credit score.

Establishing good credit takes discipline, something you should be familiar with in the military. Taking the time to build it now will hold you in good stead throughout the years and will enable you to get bigger loans when you need it. Eventually you will need a car and a home. If you have good credit you will be able to get approved for a loan more easily and get lower interest rates.

Tinggalkan Balasan